How a Mortgage Rate Buydown Works (And When It Makes Sense)

A mortgage rate buydown can lower your monthly payment. Learn how temporary and permanent buydowns work, who pays, and if it’s worth it.

If you’ve been shopping for a home in a high-rate environment, you’ve probably heard the phrase “mortgage rate buydown” thrown around. Builders offer them. Sellers offer them. Loan officers mention them in the same breath as monthly payment relief. But what does it actually mean — and more importantly, is it worth it for your situation?

Here’s a clear, no-fluff explanation of how a mortgage rate buydown works, what it costs, and how to decide if it makes sense for you.

What Is a Mortgage Rate Buydown?

A mortgage rate buydown is a financing arrangement where an upfront sum of money is paid — usually at closing — to reduce the interest rate on a mortgage loan. That reduction lowers the borrower’s monthly payment, either for a set period of time or for the entire life of the loan.

In plain terms: someone pays money now so you pay less every month.

The “someone” is usually the seller, the builder, or the lender — though buyers can pay for it themselves. And the rate reduction can be temporary (lasting one to three years) or permanent (lasting the full loan term).

Temporary Buydown vs. Permanent Buydown

The two main categories of buydowns work very differently.

Temporary Buydown

A temporary buydown reduces your interest rate for the first few years of your loan, then returns to the note rate (your original locked rate) for the remainder of the term.

The money to fund this reduction isn’t coming from thin air, it’s held in an escrow account and used each month to supplement your lower payment during the buydown period.

Temporary buydowns are most often seller-funded and are most appealing in markets where buyers expect rates to fall. The theory: get through the next few years at a lower payment, then refinance when rates drop.

Permanent Buydown (Discount Points)

A permanent buydown uses “discount points” to reduce your rate for the full loan term. One discount point equals 1% of the loan amount, and each point typically reduces your rate by 0.25% (though this varies by lender and market conditions).

A permanent buydown is paid upfront, usually by the buyer, and it permanently changes the interest rate on the loan. There’s no escrow account, no step-up period, and no expiration.

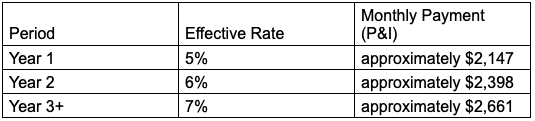

How Does a 2-1 Buydown Work?

The 2-1 buydown mortgage is the most common temporary buydown structure. Here’s how it works:

Year 1 — Your rate is 2% below the note rate

Year 2 — Your rate is 1% below the note rate

Year 3 and beyond — Your rate returns to the full note rate

Example with real numbers:

The payment in Year 1 and Year 2 is supplemented by funds in a buydown escrow account. The seller (or whoever is paying for the buydown) contributes enough at closing to cover the monthly difference across those two years.

In this example, the cost to fund a 2-1 buydown on a $400,000 loan at 7% would be roughly $14,000 to $17,000 — a significant seller concession, but one that can make a listing more competitive without simply lowering the price.

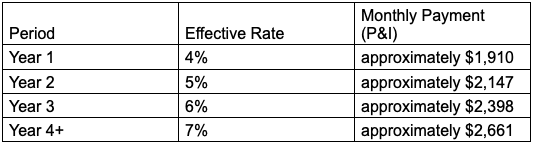

How Does a 3-2-1 Buydown Work?

The 3-2-1 buydown mortgage adds one more year to the structure:

Year 1 — Rate is 3% below the note rate

Year 2 — Rate is 2% below the note rate

Year 3 — Rate is 1% below the note rate

Year 4 and beyond — Rate returns to the note rate

Using the same $400,000 loan at 7%:

A 3-2-1 buydown is more expensive to fund and less common. It’s most often offered by home builders on new construction as a marketing incentive to attract buyers who are rate-sensitive.

Who Pays for the Buydown — the Buyer or the Seller?

In most cases, the seller or the builder pays for a temporary buydown. It’s structured as a seller concession and funded at closing. From the buyer’s perspective, it’s essentially a discount on the purchase price — just redirected toward payment relief rather than a lower sales price.

Buyers can pay for buydowns themselves, but it’s rarely the optimal use of cash. If you’re going to spend money upfront to reduce your payment, a permanent buydown (discount points) is usually a more efficient tool because the rate reduction lasts for the life of the loan.

Seller-paid temporary buydowns became popular when interest rates rose sharply because they gave sellers a tool to attract buyers without slashing prices — and gave buyers short-term payment relief.

How Much Does It Cost to Buy Down a Mortgage Rate?

For temporary buydowns, lenders calculate the cost by totaling the monthly payment difference across the buydown period.

A general rule of thumb:

2-1 buydown — costs roughly 2% to 3% of the loan amount

3-2-1 buydown — costs roughly 3% to 4% of the loan amount

For permanent buydowns, each discount point costs 1% of the loan amount. If your lender prices one point at a 0.25% rate reduction, buying your rate down from 7% to 6.5% on a $400,000 loan would cost approximately $4,000 (two points).

Always ask your lender for a break-even analysis on permanent buydowns. If the monthly savings takes 8 years to recoup the upfront cost, and you plan to sell or refinance in 5 years, it’s not worth it.

When Does a Buydown Make Sense vs. Negotiating a Lower Price?

This is the right question to ask, and the answer depends on your cash flow situation.

A price reduction lowers your loan balance, which reduces your monthly payment slightly and also reduces how much interest you pay over the life of the loan. The benefit is permanent and compounding.

A buydown reduces your monthly payment significantly in the short term — but your loan balance stays the same, and the benefit disappears when the buydown period ends.

A buydown makes more sense when:

You need near-term cash flow relief (lower payment in year one is critical to your budget)

You expect to refinance within a few years as rates fall

The seller is offering to fund it as part of the deal

A price reduction makes more sense when:

You’re planning to stay long-term

You don’t expect to refinance soon

Your cash flow is stable and the short-term payment savings don’t change your decision

Sometimes you can negotiate for both — a modest price reduction and a seller-funded buydown.

Can a Buydown Be Used on FHA, VA, or Conventional Loans?

Yes, buydowns are available across all major loan types, though there are some differences.

Conventional loans — Temporary and permanent buydowns are both available. Seller concession limits depend on your loan-to-value ratio.

FHA loans — Temporary buydowns (including 2-1 buydowns) are allowed. Seller concessions are capped at 6% of the sales price.

VA loans — Temporary buydowns are allowed. VA considers a seller-funded buydown to be a seller concession, subject to the 4% concession cap (though eligible closing costs that fall under concessions are calculated separately — check with your lender).

Each loan type has specific rules. If you’re using a government-backed loan, confirm the structure with your lender before negotiating a buydown into the purchase contract.

What Is a Discount Point and How Does It Relate?

A discount point is simply the mechanism behind a permanent buydown. When you buy discount points, you’re prepaying interest to the lender in exchange for a lower rate.

One point = 1% of the loan amount.

The rate reduction per point varies by lender, market conditions, and loan type — typically 0.125% to 0.375% per point. Your lender should be able to show you the exact pricing at the time of your rate lock.

Discount points are tax-deductible in many cases (consult a tax advisor), which can improve the math for buyers who plan to stay long-term.

Is a Mortgage Buydown Worth It Right Now?

In a high-rate environment, a seller-funded temporary rate buydown can be a genuinely useful tool — especially if you believe rates will come down and you’re planning to refinance in the next two to three years. You get meaningful monthly payment relief while you wait.

The risk is simple: if rates don’t fall, you lose the benefit of the buydown when the period ends and your payment steps up to the full rate. You need to be financially prepared for that higher payment.

For buyers paying out of pocket for a permanent buydown, the calculus is stricter. Run the break-even math before committing. How long do you need to stay in the home for the upfront cost to pay off in monthly savings? If that timeline aligns with your plans, it may be worth it.

The bottom line: a mortgage rate buydown is a tool, not a magic fix. It works best when used intentionally, negotiated strategically, and understood fully before you commit.

Ready to sell your home as-is? We make the process simple and stress-free! At Elevated Home Solutions, we buy homes in any condition, offering a fast and fair cash offer without the need for repairs. Skip the hassle of traditional listings and sell your home as-is today. Contact us now to get started!